Non-IAB Members can access the Executive Summary and IAB Members can access the full report in the “Downloads” section below

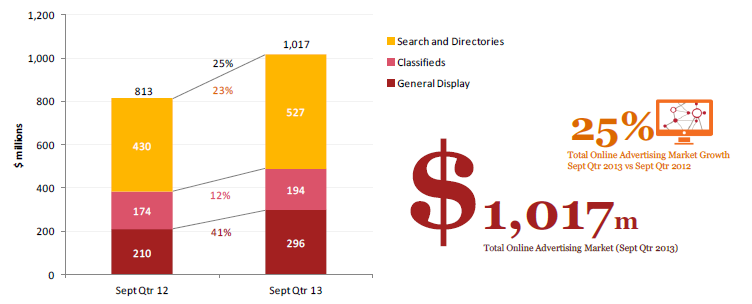

Sydney, Australia, 18th November 2013: Online advertising has continued its strong growth, exceeding $1bn in the September 2013 quarter while recording 25 percent growth year on year from September 2012 and 4.6 percent on the prior quarter according to IAB Australia’s Online Advertising Expenditure Report (OAER) which is produced by PricewaterhouseCoopers (PwC) and was released today.

Display advertising was the biggest growth area according to the Report, recording 41 percent growth year on year to reach $295.6m in the September 2013 quarter, while Classifieds recorded $193.7m and Search and Display $527.4m. Search and Display now represent 52 percent of the total online advertising market, general display 29 percent; and classifieds 19 percent share.

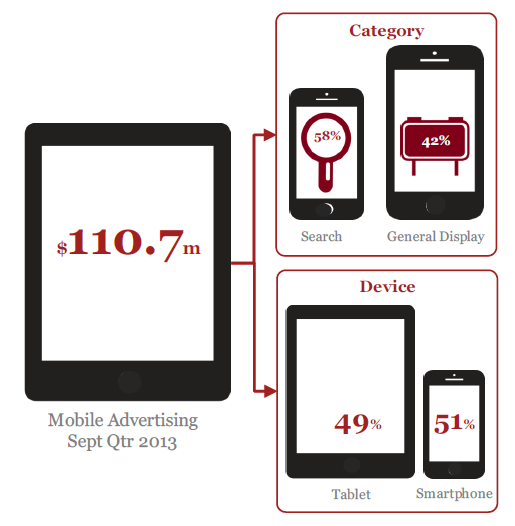

Mobile advertising reported significant growth for the September quarter and now represents 11 percent of the total online advertising market. Within the mobile advertising expenditure of $110.7m, 58.4 percent was search and 41.6 percent was general display. Device category shares were relatively equal with smart phones at 51.4 percent and tablets at 48.6 percent.

Video advertising expenditure doubled year on year, recording $43.1m for the September quarter and it now represents 15 percent of the total display advertising market.

The IAB Report follows the recently released data from CEASA that noted in the January to June 2013 period, online advertising represented 28.6 percent of the total advertising market.

Alice Manners, CEO of IAB Australia commented: “This report and the recent CEASA data confirm that the overall health of the online advertising market is very robust. We expect that by the end of this calendar year the online advertising sector will exceed 30 percent of the total advertising market.

“Digital is now an accepted and integral component of advertising and is being embraced by a broad range of advertisers. As advertising formats and approaches evolve and our ability to deliver full transparency and accountability continues to improve, there is no doubt that growth will continue and we expect that by the end of this year marketers will be spending around one third of their total budgets on digital advertising,” said Ms Manners.

Gai Le Roy, Director of Research for IAB Australia added: “In September we released the results of our State of the Video Industry Report with Adap.tv which found that nine out of 10 agencies and marketers had increased their video ad spend over the past 12 months, while 60 percent of ad buyers were buying mobile video ads. Today’s PwC Report shows that mobile and video continues to captivate advertisers and we expect to see the growth in these sectors maintained for some time to come.”

The Federal Election saw political parties embracing online advertising last quarter resulting in doubling in spend which saw the Government/Political sector responsible for six percent of display advertising. The auto sector remains the highest spending industry category for display advertising, while spending in the finance sector dropped slightly and real estate increased to almost 10 percent share – an increase of 8.8 percent on the same quarter in 2012 driven in part by the strong residential property market.

Online Advertising Expenditure compared to prior comparative quarter (September Qtr 2012)

Mobile Category and device share (September Qtr 2013)

This Report was prepared under the “New Approach” introduced in the June Qtr 2012 OAER. The data collected from industry participants has been supplemented by:

- Estimates for Google display, video, and mobile advertising as well as estimates for Facebook display and mobile advertising

- Refinement of prior methodology used for estimating Google search; and

- Historical mobile advertising data collected from industry participants from March Qtr 2011 combined with estimated Google mobile advertising, to provide a picture of the aggregated mobile advertising market and the growth trends.

Comparative data for the period from September Qtr 2010 has been restated to be consistent with the methodology changes. From time to time, estimated revenues are updated as new information and data sources become available. This may cause a series break in the data and should be taken into account when considering historical trends.